ESG investments sector was referred to as ‘rife with greenwashing’ recently in the Financial Times (FT) article. These concerns not only diminish trust in institutions and the system as a whole but, most significantly, pose a danger to the socio-economic and environmental challenges we are trying to solve. From health crises to inequality, biodiversity loss to climate change, sustainable behaviour should always begin with the end goal in mind.

Responsible businesses are under the magnifying glass due to the myriad of ways sustainability performance of companies is accounted for. The FT mentions that the desire to get beyond ‘greenwashing’ ‘has accelerated the drive for sustainability standards. However, there is misinformation around what the distinction is between standards, frameworks, ranking and ratings, and their differences in approach and purpose.

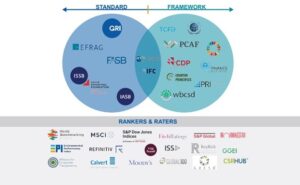

Clearing up the vocabulary

The sustainability landscape can be grouped in roughly two main directions: organizations that publish standards and the ones that issue frameworks or guiding principles. Of course, the world is not entirely black and white as some organizations tend to do both.

Standards

Standards are the agreed level of quality requirements, that people think is acceptable for reporting entities to meet. A standard can be thought of as containing specific and detailed criteria or metrics of ‘what’ should be reported on each topic. In general, corporate reporting standards have in common the following features: a public interest focus, independence, due process, and public consultation, generating a stronger basis for the information being asked.

Frameworks

Frameworks on the other hand provide the ‘frame’ to contextualize information. Frameworks are those that are normally put into practice in the absence of well-defined standards. A framework allows for flexibility in defining the direction, but not the method itself. A framework can be thought of as a set of principles providing guidance and shaping people’s thoughts on how to think about a certain topic but miss a defined reporting obligation.

Both standards and frameworks derive authority from either being mandatory by law or being endorsed by a majority of (relevant) stakeholders, for example through peer-group or investor pressure to use them.

Finally, there are ratings and rankings that capture a ‘score’ of the maturity or ESG savviness of organizations. A company’s ESG rating is comprised of a quantitative score and a risk category. The information that is disclosed based on reporting standards and frameworks provides important input into the activities of rankers and raters. However, what the actual rating is comprised of is often a black box. Nevertheless, the importance of ranking and ratings, especially regarding access to finance, is increasing. We will cover this topic in more depth in a future GRI Perspective.

Applying due process

A global corporate reporting leader at Deloitte once said: “To be effective, the standards will need to be brought into regulation around the world, together with associated enforcement, monitoring, governance and controls, assurance, and training.”

Precisely the associated ability of enforcement is the distinctive feature of a standard. Compared to frameworks, standards are more rigid and thorough. The GRI Standards are developed according to a formally defined Due Process Protocol, providing requirements for developing a standard, which is overseen by an oversight committee.

The protocol ensures the Standards are developed following a transparent and multi-stakeholder process. Experts including business, civil society, labour, investment institutions, academics and accountants around the world are involved, through a consensus-seeking approach that draws on their diverse backgrounds and expertise.

GRI’s Global Sustainability Standards Board (GSSB) routinely conducts public comment periods to gather stakeholder feedback on draft Standards. There is a broad consensus between stakeholders on what adequate reporting on sustainability topics should look like. That is the beauty of GRI’s due process, due to the multi-stakeholder approach.

Developments in sustainability reporting standards

While there is a multitude of frameworks that deal with the topic of sustainability, there are currently on a global scale only two reporting standards: GRI and SASB each with a different audience and scope. The world of sustainability reporting is however changing. There are currently two notable developments happening in the sustainability reporting landscape:

- The European Sustainability Reporting Standards (ESRS) being created by the EU will be based on double materiality, for a multi-stakeholder audience (which includes investors). GRI and the European Financial Reporting Advisory Group (EFRAG) are leading its co-construction efforts.

- Standards for the disclosure of sustainability-related financial information are being drafted by the IFRS Foundation – with which the newly established International Sustainability Standards Board (ISSB) is charged with – and will be based on financial materiality for an investor audience only.

In our view, the approaches of the IFRS and the EU are not competing but complementary forces. Different purposes for different audiences with different standards. Standards with a sole purpose to inform investors are built on a different concept from impact standards that inform a broader group of stakeholders. The GRI Standards are the only global standards with an exclusive focus on impact reporting for a multi-stakeholder audience – making it an essential factor in the shaping of a reporting structure.

As such, GRI has a key role in working with EFRAG and the ISSB to build this comprehensive global set of sustainability reporting standards. Only then the two-pillar structure can be created – for financial and sustainability standards – with a core set of common disclosures and each pillar of equal footing. Covering the information needs of investors as well as other stakeholders will increase confidence and credibility in the sustainability behavior of companies.

GRI will cooperate with EFRAG, the ISSB, and (inter) governmental organizations to drive sustainability disclosure in a two-pillar reporting structure. Credibility is created through accountability. And accountability can only be provided through transparency. Frameworks without a definite reporting obligation cannot fulfil this purpose – but publishing relevant information based on widely used truly global corporate reporting standards underpinning both the financial and impact materiality perspective – will.